Rotorua's property sales have slumped. Photo /Andrew Warner.

Rotorua's property sales have slumped. Photo /Andrew Warner.

Bay of Plenty residential and lifestyle property sales have plummeted by 41.6 per cent in one year and some real estate agents have exited the industry off the back of the “tough” market.

A rapid rise in interest rates is believed to have had a big impact and the boss of the biggest agency in the Bay said properties were taking longer to sell and pricing was back by about 10 per cent. Another said some people who were highly leveraged may look to sell off their holiday home and first-home buyers could benefit, as deposits would be less than what they were previously.

A OneRoof-Valocity Year in Review published today reveals that to the year ending in October in the Bay of Plenty, residential and lifestyle properties sales fell by 41.6 per cent to 4130. Included in those figures were 1173 first-home buyers and 1182 investors, with those categories buying 32.2 per cent and 49.6 per cent fewer properties respectively over the same timeframes.

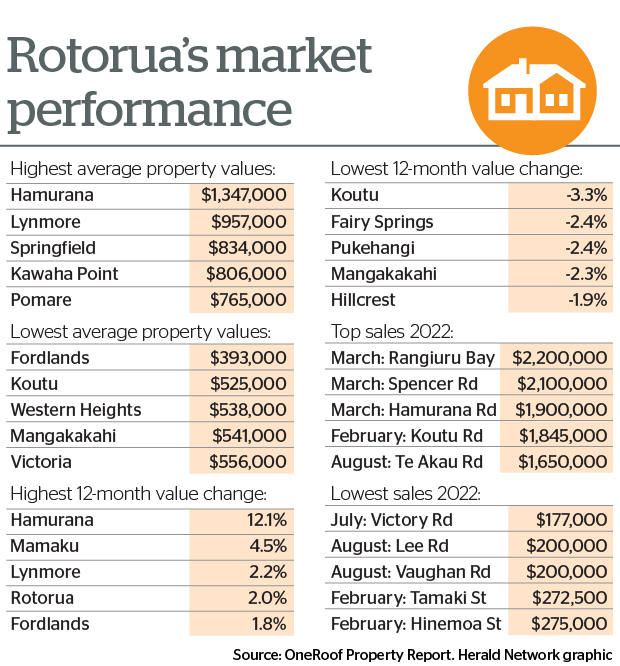

In Rotorua, a snapshot shows the average median house price fell $101,100 from a peak of $821,900 in April to $720,800. The biggest sale was a house in Rangiuru Bay Rd, Lake Tarawera, which fetched $2.2 million while the lowest was a house that sold in Victory Rd, Fairy Springs, in July.

Hamurana had the highest suburb average property value at $1.34m while Fordland was the lowest at $393,000.

Managing director of the Realty Group, which operates Eves and Bayleys, Heath Young, said the recent rapid rise in interest rates to combat inflation has had a big impact on property trading volumes.

“This has resulted in property taking longer to sell and pricing to be back approximately 10 per cent when compared to values from a year ago.”

He said all traditional sectors were still buying and selling, with noticeably more first-home buyers replacing the reduced investor activity.

“If you are looking to sell and buy in this market for the purposes of upsizing, downsizing or moving within the region then it is certainly a good time, as any value reduction in your own property made on the sale is matched by the fact that it is also costing less when you purchase.

“Across our branches, we are back 10 to 20 per cent on volumes transacted compared to last year.”

Young said there were certainly agents leaving the industry.

“It is clear that those agents that recently come into the industry over the past couple of years have a higher representation when analysing those leaving the industry at the moment.”

Ray White Rotorua business owner and principal Jacqueline O’Sullivan. Photo / Supplied

Ray White Rotorua business owner and principal Jacqueline O’Sullivan said the number of properties on the market increased to almost double that of last year, which had in turn given buyers more choices, resulting in the median days to sell increasing.

“We have also seen more offers being made subject to the purchaser’s own home selling, thus further slowing the market. More choice of properties on the market may have also contributed to the decrease in house sale prices.”

She agreed that the downward movement in the number of sales could be attributed to the uncertainty of the interest rates and how high these might go, which had also created some fears of a recession.

“Credit availability is tight and tax rules have put off some investors. Social issues have also had an impact on sales in Rotorua over the past couple of years, particularly in the Glenholme area.

“We are seeing more first-home buyers than investors in the market currently.”

O’Sullivan said the number of homes the firm had sold had dropped.

“They have fallen, we are sitting at 22 per cent so very much in line with everyone else.”

There was no doubt that some agents would leave the market, she said.

“Marketing expenses have risen significantly - along with everything else. There are agents that have never experienced a tough market and so they may take on part-time jobs to see them through this period.”

Her agency was anticipating a more challenging 2023.

“But reports are suggesting that financial pressures will ease in 2024 when interest rates are reportedly set to come down again.”

Rotorua Professionals McDowell Real Estate principal and auctioneer Steve Lovegrove. Photo / Andrew Warner

Rotorua Professionals McDowell Real Estate principal Steve Lovegrove said it had been a whitewater year of ups and downs.

“It hasn’t been smooth sailing. We started with a relatively confident market at the beginning of the year and now as we enter the end of the year it’s completely the polar opposite.

“The market has gone in anecdotal terms from one property for sale with 10 buyers to 10 properties with one buyer. There are buyers but they are now more acutely aware they have choice and they have no sense of urgency like they had a year ago.”

It had seen some spectacular sales and some that had not reached the prices it had expected.

Appraising the value of a house was also proving difficult.

“We cannot accurately predict what a house will sell for. There has been no rhyme or reason to what is actually happening and now we are beginning to see the effects of the higher interest rates and higher cost of money.”

It was also seeing two types of vendors, “those who are hanging on for dear life for that high price” and those who just want their house sold.

Lovegrove said some people who had pushed the envelope to add to their property portfolio might look to sell in the new year to reduce debt.

“There could be some downsizing going on or they will be looking for other options. In Rotorua, we might see some rolling through the summer with Airbnb options to try and get some holiday income to mitigate those increasing costs.”

Falling house prices could provide opportunities for first-home buyers and if they planned to stay in the house for five, six or seven years they’d probably be sitting on the other side of the cycle.

Its sales volumes at its branches had fallen by 20 to 30 per cent but Lovegrove remained optimistic about the future.

Valocity head of valuations James Wilson said it was important to note when sales volumes were low it was very difficult to actually pick up what was going on in the market.

“Has every entire property gone down in value across the board at the same level? The answer is no.”

He said Rotorua previously had investors who were really active but that had changed.

“There were a lot who were competing against each other to buy and they paid good premiums. The rental yields in Rotorua have always been quite good but now they aren’t as healthy as they used to be.”

Some smaller investors who were focused on cash flow and couldn’t ride out losses for long had exited the market.

“We aren’t seeing that on a big scale but it’s something we are watching closely.”

Wilson said Valocity did not believe there would be a huge summer surge in sales volumes, and activity was likely to stay low.

However, in his view, at the moment nothing indicated sales values would get significantly worse as the Reserve Bank of New Zealand had been really clear about the Official Cash Rate and the banks were factoring that in.

“You’d be under a rock if you weren’t aware interest rates are only going one way.”

OneRoof editor Owen Vaughan said the property market was headed into ‘’uncharted territory’' next year and ‘’we haven’t hit the bottom yet’'.

‘’Depending on where inflation sits at the end of this quarter it will really determine how much further we have to go.’’

An ANZ spokeswoman said generally when the housing market slows, home loan applications tend to fall as well.

As a responsible lender it was important its customers can effectively manage their lending once they’re in their homes, she said.

This means collecting the right level of information from customers to ensure suitability and affordability of any lending.

A Kiwibank spokeswoman said most customers would have at least a 20 per cent deposit.

‘’As well as looking at the deposit amount and how much someone earns, Kiwibank considers the stability of the customer’s income. Whether the deposit was gifted or saved, what other debts they might have, what they spend, and the ability of the borrower to repay the loan at a higher interest rate but that might reasonably be expected over the term of the loan.’’